If your business needs funds to address a shortfall or seize an opportunity before it slips away, a working capital loan from Liquidity Solutions could be the answer. Cash flow challenges can arise from many sources, such as seasonal fluctuations, unpaid invoices, necessary repairs, or unexpected bills. Even a full order book can strain your cash flow as you rush to purchase stock and pay staff for overtime. That’s why countless UK businesses rely on working capital loans to bridge the gap, providing the financial support they need to grow or manage expenses effectively.

What is a Working Capital loan?

1. Short-Term Working Capital Loan: A loan designed to cover immediate operational expenses such as payroll, stock, and day-to-day expenses, typically with a repayment period of up to 12 months.

2. Revolving Line of Credit: A flexible credit line where businesses can borrow, repay, and borrow again up to a pre-approved limit, helping them manage ongoing working capital needs.

Advantages of Working Capital Loans

Improved Cash Flow: Provides businesses with immediate funds to cover day-to-day expenses, helping maintain smooth operations without disruptions.

Flexible Repayment: Options like revolving credit allow businesses to borrow as needed and repay based on their cash flow, offering more control over finances.

Quick Access to Funds: Working capital loans are typically easier and faster to obtain, allowing businesses to address urgent financial needs or take advantage of opportunities quickly.

If your cash flow is tied up while waiting for customers to pay or funds to clear, short-term finance could help you bridge the gap. Working capital loans are designed for businesses that have money on the way but are facing a temporary shortfall. For instance, seasonal businesses often experience income concentrated during specific times of the year.

Without sufficient working capital, your business might struggle to:

Pay your suppliers

Buying heavy equipment

Acquire plant machinery

Invest in vehicles like cars, vans, and lorries

Upgrade computer systems

Buy manufacturing or office equipment

You might even face challenges shipping and delivering orders, which could delay getting paid. A working capital loan can help you manage your finances, ensuring you have the funds to maintain operations and smooth out income fluctuations.

Business A: Clothing Retail Store

(illustration purposes only)

Business Profile: A fashion retailer with a brick-and-mortar store, specialising in seasonal collections.

Working Capital Loan Need: Business A needs working capital to purchase stock for the upcoming season and maintain cash flow for operational expenses.

Loan Type: Short-Term Working Capital Loan

Loan Details:

Loan Amount: £30,000

Repayment: £2,582 per month for 12 months

Interest Rate: 6%

Total Repayment: £30,984 (including interest)

Scenario:

Business A secures the loan to purchase additional stock for the upcoming season and to cover payroll and other operational costs.

Monthly repayments of £2,582 are made from sales revenue, ensuring the store has enough stock to meet demand.

After 12 months, the loan is fully repaid, and the store sees increased revenue due to well-stocked shelves.

Business B: Family-Owned Restaurant Business

(illustration purposes only)

Business Profile: A popular family-owned restaurant in a busy area, known for its high-quality food and great customer service.

Working Capital Loan Need: Business B needs a working capital loan to cover fluctuating cash flow during off-peak months and ensure smooth operations.

Loan Type: Revolving Line of Credit

Loan Details:

Credit Limit: £20,000

Repayment: Interest-only payments on the amount drawn

Interest Rate: 8%

Monthly Interest Payment (if fully drawn): £133

Term: 12 months

Scenario:

Business B uses the revolving line of credit to cover payroll and supplier payments during slower months.

As customer payments come in, the loan is repaid, and the credit line remains available when needed.

The restaurant maintains smooth operations year-round without worrying about cash flow issues during off-peak periods.

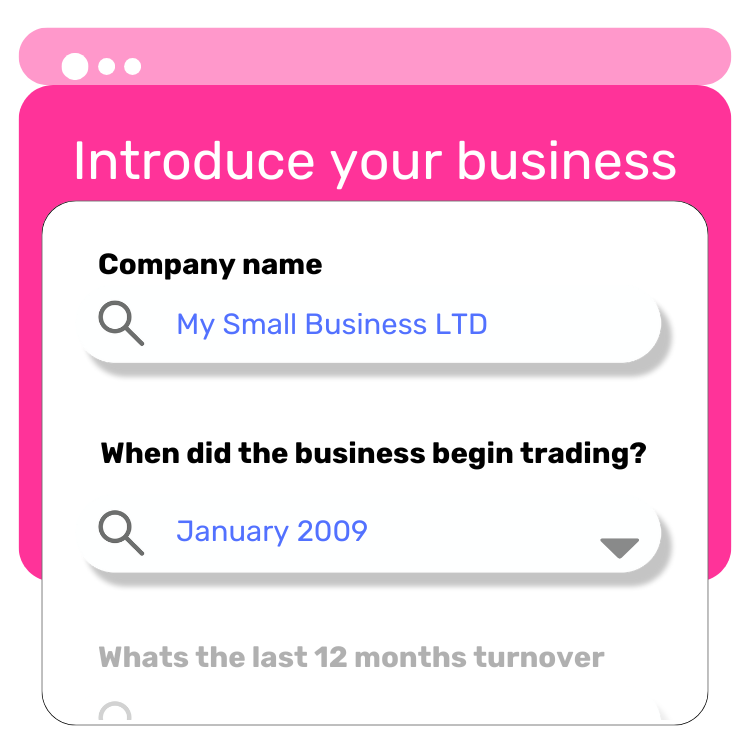

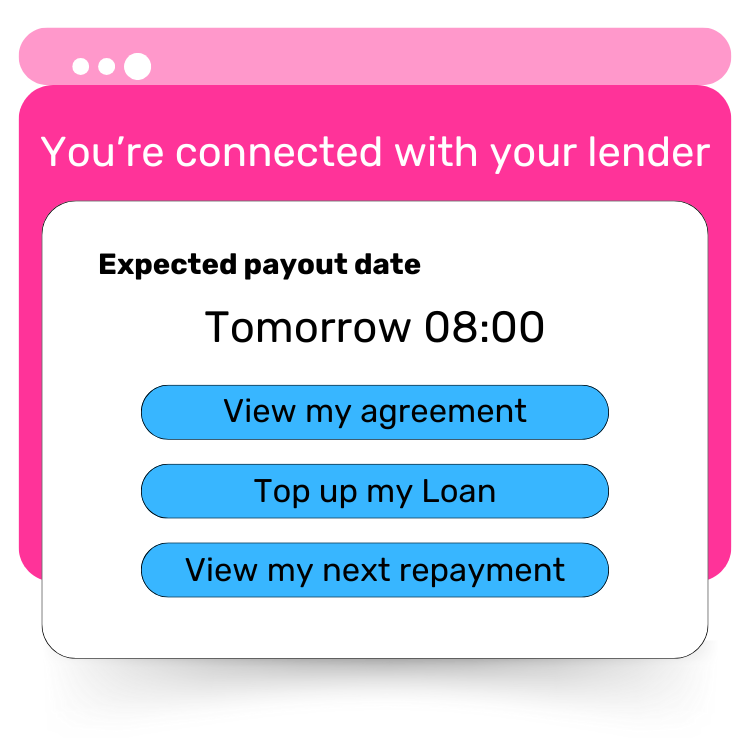

How does a Liquidity business loan work?

1

Apply Online

Start by submitting your application on our website, quick and easy!

2

We Search for the Best Lender

We scan our panel of trusted lenders to find the one that best fits your needs.

3

Connect with Your Lender

We introduce you to the lender, and they’ll take it from there to complete your application. You could get funds in as little as 24 hours.

Options for Increasing Your Working Capital

Overdrafts

If your business already has an overdraft facility, you can access additional funds by dipping into your account’s credit limit. However, setting up a new overdraft can take time, so this option may not be ideal if you need funds immediately. Keep in mind that overdrafts often come with fees and penalties.

Business Credit Lines

A business credit line functions similarly to an overdraft. You agree on a borrowing limit with your lender and can draw as much or as little as needed, paying interest only on the amount borrowed. Credit lines are a flexible option if you’re unsure about the exact amount you require.

Business credit cards are a convenient way to manage monthly cash flow and access extra funds when needed. However, interest rates on credit cards can be higher than those on other short-term or working capital loans.

This involves raising funds by selling shares of your business to investors. In return, investors gain partial ownership and a share of future profits. Unlike debt financing, equity financing doesn’t require repayment, which can ease cash flow pressures. However, it does dilute your ownership stake, so it’s essential to evaluate the trade-offs before proceeding.

A working capital loan is a short-term financing solution that helps UK businesses manage day-to-day expenses like purchasing stock, paying salaries, and covering bills, ensuring smooth cash flow.

How does a working capital loan work?

When a business in the UK applies for a working capital loan, the lender evaluates its financial health, credit rating, and ability to repay the loan. Based on this assessment, the lender decides the loan amount, interest rate, and repayment terms. After approval, the borrower receives the funds, which are typically repaid in regular installments over a short duration.

How can a working capital loan help my business?

A working capital loan helps bridge cash flow gaps, cover operational expenses, and capitalise on growth opportunities. It enables businesses to acquire stock or raw materials, manage seasonal revenue fluctuations, take advantage of supplier discounts through early payments, and enhance credit scores by ensuring timely repayments.

What are the requirements to qualify for a working capital loan?

Lenders assess factors such as the business’s financial stability, credit rating, time in operation, revenue, profitability, and the owner’s credit history and personal financial health.

How much can I borrow with a working capital loan?

The amount you can borrow with a working capital loan depends on your business’s financial health, revenue, credit rating, and the lender’s assessment. These loans are usually smaller than long-term loans, typically ranging from a few thousand to several hundred thousand pounds.

What is the interest rate for a working capital loan?

The interest rate for a working capital loan depends on factors like the lender, the borrower’s credit rating, loan amount, and term. Rates are usually higher than long-term loans since they cater to short-term financial needs.

How long is the repayment period for a working capital loan?

The repayment period for a working capital loan is generally short, ranging from a few months to a couple of years. Since these loans are intended to meet short-term financial needs, the repayment period is aligned with the time it takes for the business to generate sufficient cash flow to repay the loan.

Can I get a working capital loan if I have bad credit?

While bad credit can make it harder to qualify for a working capital loan, some UK lenders specialise in funding businesses with weaker credit histories. However, this may come with higher interest rates and stricter repayment terms.

How quickly can I get approved and receive the funds?

The approval and funding timeline for a working capital loan can vary depending on the lender and the complexity of the application. Some lenders offer fast and streamlined application processes, with funds being disbursed within a few days of approval.

Can I use a working capital loan for any business expenses?

Yes, working capital loans are generally flexible and can be used for a variety of business expenses. This includes paying for stock, covering payroll, settling bills, funding marketing efforts, and other essential operational costs.

What documents do I need to apply for a working capital loan?

The required documents vary by lender but typically include business registration documents, financial statements, bank statements, tax returns, and proof of identity for the business owner(s).

Are there any fees or charges associated with a working capital loan?

Yes, working capital loans may come with various fees and charges, including origination fees, processing fees, and early repayment fees. It is important to carefully review the loan’s terms and conditions to fully understand all applicable fees.

Can I use a working capital loan to consolidate my debts?

Yes, in some cases, you may be able to use a working capital loan to consolidate your debts. However, it’s important to check with the lender to confirm if debt consolidation is allowed. Some lenders may have specific restrictions on how the loan funds can be used.

Can I get a working capital loan if I am a start-up business?

It can be more difficult for start-up businesses to qualify for a traditional working capital loan from banks or financial institutions, as lenders typically prefer businesses with a history of revenue and stable cash flow. However, there are alternative lenders and financing options specifically designed for start-ups, which may have more flexible eligibility criteria.

Can I get a working capital loan if my business has irregular cash flow?

The possibility of securing a working capital loan with irregular cash flow depends on the lender and their risk evaluation. Irregular cash flow can be viewed as a risk, as it may impact your ability to repay the loan on time. While traditional lenders may be hesitant, some alternative or online lenders might be more flexible and consider other factors when reviewing your application.

Can I use a working capital loan to expand my business?

Yes, a working capital loan can be used to fund business expansion. Whether you’re opening a new location, launching a new product, or investing in marketing campaigns, a working capital loan can provide the necessary funds to support growth opportunities.

How do I choose a reputable lender for a working capital loan?

When choosing a lender for a working capital loan, consider their reputation, interest rates, fees, and repayment terms. Ensure they offer the loan amount you need and that you meet their eligibility criteria. Look for transparent terms and excellent customer service to support you throughout the loan process.

What happens if I cannot repay the working capital loan on time?

Failing to repay a working capital loan on time can result in late fees, penalties, and a negative impact on your credit rating, making future financing more difficult. Lenders may take further action if payments are missed. If you’re struggling, it’s important to communicate with your lender to explore solutions like refinancing or adjusting the repayment schedule.

Are there alternative financing options for working capital needs?

Yes, several alternative financing options are available for working capital needs, especially if traditional lenders aren’t a good fit. These include business lines of credit, which provide flexible access to funds, invoice financing to unlock cash from unpaid invoices, merchant cash advances based on future card sales, and online lenders that cater to businesses with varying credit profiles.

Can I use a working capital loan to buy stock or equipment?

Yes, you can use a working capital loan to purchase inventory or equipment for your business. These loans are commonly used for short-term financing needs, such as restocking inventory, buying new equipment, or covering day-to-day operational expenses. Be sure to confirm with the lender that the loan can be used for these purposes and that the investment will contribute to your business’s growth and profitability.