Invoice finance is a funding solution that allows businesses to unlock cash tied up in unpaid invoices. Instead of waiting for customers to pay, businesses can sell or borrow against their invoices through a finance provider. This helps improve cash flow, support working capital needs, and keep operations running smoothly.

What is Invoice Finance?

There are two primary types of invoice finance:

Invoice Factoring: The finance provider purchases the invoices, advances a percentage (usually 70%-90%) of their value upfront, and takes over the responsibility of collecting payment from the customers.

Invoice Discounting: The business retains control of the customer relationship and debt collection, while the finance provider lends a percentage of the invoice value as a loan.

Business Profile: A furniture manufacturer supplying custom-made office desks to large corporations.

Challenge: Business A offers 60-day payment terms to corporate clients. While waiting for payments, the company struggles to pay its suppliers and workers on time, slowing down production.

Solution: The company uses invoice factoring. Once invoices are issued for completed orders, the factoring company advances 85% of the invoice value immediately. This allows Business A to cover operational costs and keep production on track.

Benefits for Business A:

Quick access to funds to pay for raw materials and labour.

No more waiting 60 days for customer payments.

The factoring company handles collections, reducing administrative effort.

Business B: A Digital Marketing Agency

(illustration purposes only)

Business Profile: A digital marketing agency working with small and medium-sized businesses. It offers comprehensive campaigns billed monthly, with clients given 30-day payment terms.

Challenge: Business B needs to pay its freelancers and advertising platforms upfront, but client payments are delayed.

Solution: The agency uses invoice discounting. For each invoice issued, the finance provider advances 80% of the value. Once the client pays the invoice, the agency repays the loan minus a small fee.

Benefits for Business B:

Maintains strong cash flow to pay freelancers and cover expenses.

Retains control of customer relationships and collections.

Provides flexible and quick access to working capital.

Why use Invoice Financing

Invoice finance can be a valuable tool for improving cash flow and managing working capital, but like any financial product, it is always best to review if it is the best finance option for you and your business. Here’s a detailed breakdown:

Improved Cash Flow

Quick Access to Funds

Supports Business Growth

Flexible Financing

No Additional Collateral Required

Outsourced Credit Control (Factoring only)

Reduces Risk of Bad Debts (Non-recourse factoring)

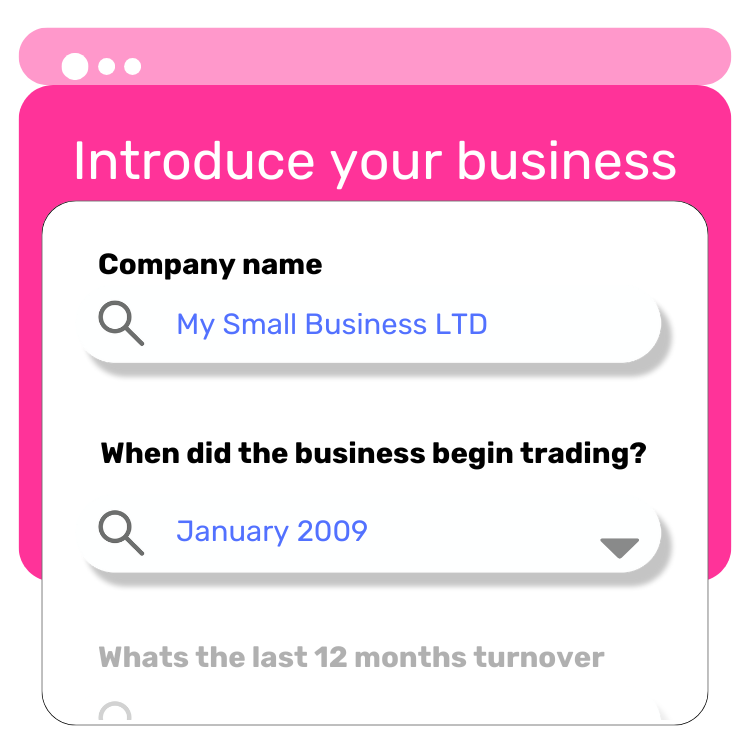

Start by submitting your application on our website, quick and easy!

2

We Search for the Best Lender

We scan our panel of trusted lenders to find the one that best fits your needs.

3

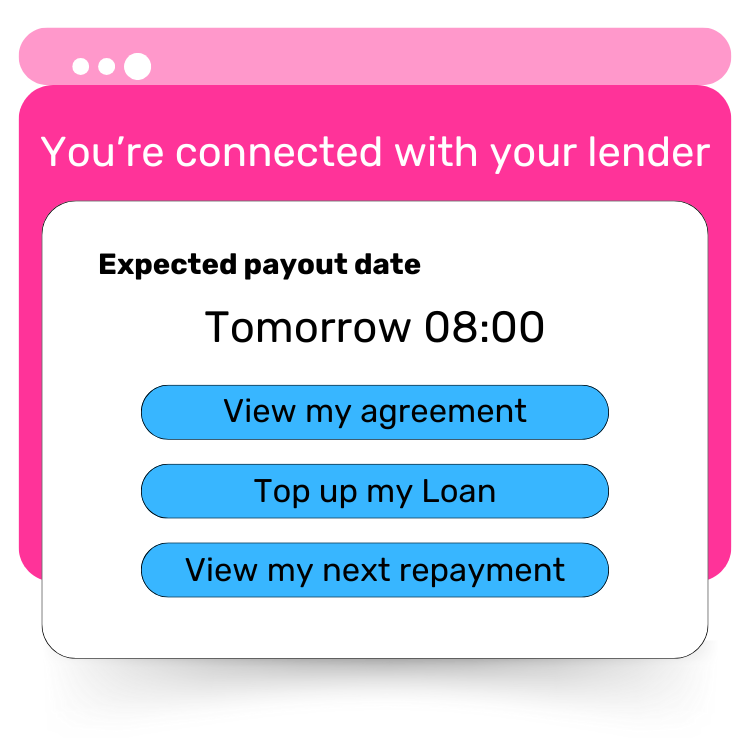

Connect with Your Lender

We introduce you to the lender, and they’ll take it from there to complete your application. You could get funds in as little as 24 hours.

Business Loans

What is Invoice Finance?

Invoice Finance is a funding solution where businesses sell their unpaid invoices to a lender or financier to access a percentage of the invoice value immediately, improving cash flow.

How does Invoice Finance work?

Once you issue an invoice to a customer, the lender advances you a portion of the invoice amount (typically 70-90%). When the customer pays the invoice, the lender deducts their fees and releases the remaining balance to you.

How can Invoice Finance help my business?

Invoice Finance can improve cash flow, reduce payment delays, and provide working capital to pay suppliers, meet payroll, or fund growth without waiting for customers to pay.

What are the requirements to qualify for Invoice Finance?

Requirements typically include having creditworthy customers, outstanding invoices, and a track record of reliable invoicing practices. Lenders may also assess your financial health and industry.

How much can I borrow with Invoice Finance?

The borrowing limit depends on the value of your outstanding invoices. Lenders generally advance 70-90% of the invoice amount upfront.

What is the interest rate for Invoice Finance?

Rates vary depending on the lender, your industry, and the risk involved. Fees typically include a service fee (1-3%) and an interest rate on the advanced funds, often ranging from 1-5%.

Can I use Invoice Finance to consolidate my debts?

No, Invoice Finance is specifically designed to release funds tied up in unpaid invoices, not for debt consolidation.

Can I get Invoice Finance if I am a start-up business?

Yes, invoice finance can be a good option for start-ups with unpaid invoices, as approval is based on customer creditworthiness rather than the business’s financial history.

How long is the repayment period for Invoice Finance?

Repayment depends on the terms of your invoices. Typically, the finance is settled when the customer pays their invoice, which is often within 30 to 90 days.

Can I get Invoice Finance if I have bad credit?

Yes, lenders focus more on the creditworthiness of your customers than on your own credit rating. However, a poor credit history might affect the fees or terms offered.

How quickly can I get approved and receive the funds?

Approval and funding are usually quick, often within 24-48 hours for established businesses. Start-ups or new clients may take a bit longer to set up.

Can I use Invoice Finance for any business expenses?

Yes, the funds can be used for any business expenses, including paying suppliers, covering payroll, or investing in growth opportunities.

What documents do I need to apply for Invoice Finance?

You’ll need copies of unpaid invoices, customer details, proof of business identity, and possibly financial statements.

Are there any fees or charges associated with Invoice Finance?

Yes, fees may include a service fee (a percentage of the invoice value), interest on the advance, and additional charges for certain services, such as customer credit checks.

Can I get Invoice Finance if my business has irregular cash flow?

Yes, Invoice Finance is specifically designed to support businesses with irregular cash flow caused by delayed customer payments.

Can I use Invoice Finance to expand my business?

Yes, the improved cash flow from Invoice Finance can be reinvested into your business for expansion, hiring staff, or purchasing stock.

How do I choose a reputable lender for Invoice Finance?

Research lenders’ reviews, compare fees and terms, and ensure they have experience in your industry. Look for transparent pricing and customer support.

What happens if my customer doesn’t pay the invoice?

If your customer doesn’t pay, you may need to repay the advance yourself, depending on the type of Invoice Finance. Non-recourse finance protects you from this risk, while recourse finance holds you responsible.

Are there alternative financing options for managing unpaid invoices?

Yes, alternatives include invoice discounting, accounts receivable financing, and traditional business loans.

Can I use Invoice Finance if my invoices are disputed?

No, most lenders will not advance funds on disputed invoices. Only invoices with clear payment terms and no issues are eligible.